For most business owners, VAT is one of those things that gets dealt with and moved on from. But when a payment is missed or delayed, the consequences can escalate more quickly than most people realise. However, the way HMRC’s penalty system is structured means the costs can feel like they’re coming from every direction at once.

This post breaks down exactly how the system works, what to expect if a payment falls overdue, and (most importantly) what you can do to protect yourself and your business.

How HMRC's VAT Penalty System Actually Works

The penalty system has a few moving parts, so it’s worth understanding each one clearly.

Interest — From Day One

From the moment a VAT payment becomes overdue, interest starts accruing. The rate is 4% plus the Bank of England base rate, applied to the outstanding balance until the full amount is cleared. There’s no grace period for interest, it begins immediately and continues until the debt is settled in full.

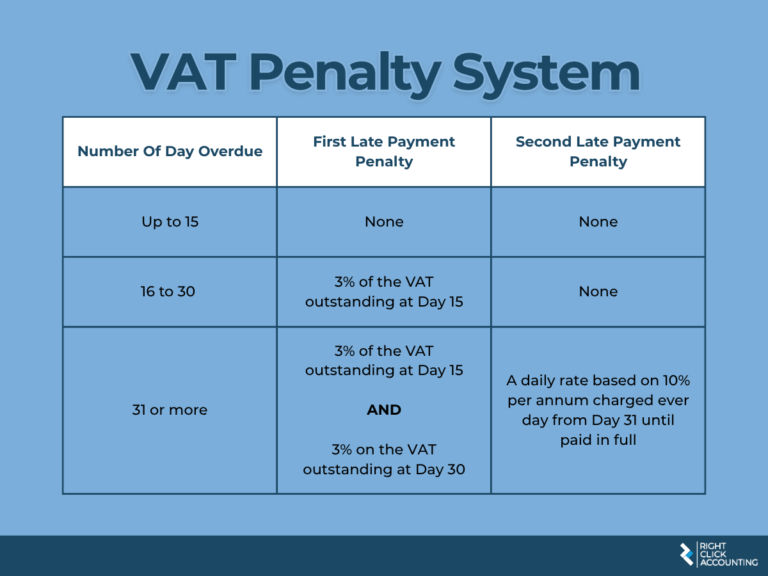

The 15 Day Window

If you pay within 15 days of the due date, no penalty is applied. You’ll still owe the interest that has accrued, but there’s no additional penalty charge. This window exists but it’s tight, and it’s easy to miss if cash flow is under pressure.

Day 16 to day 30 — First Late Payment Penalty

If payment is made between 16 and 30 days after the due date, HMRC applies the first part of the late payment penalty which is 3% of the outstanding VAT amount. At this stage it’s a one-off charge, but it sits on top of the interest that has been running since day one.

Day 31 and beyond — Where It Gets More Complex

This is where the system becomes significantly more costly, and where many business owners are caught off guard.

Once a payment reaches 31 days overdue, two things happen simultaneously:

A second part to the first late payment penalty is applied, an additional 3% of the VAT amount outstanding. So at this point you’re looking at 6% in first penalty charges alone, on top of accruing interest.

A second late payment penalty is also introduced and is calculated at 10% per annum on the outstanding balance, running until the overdue amount is fully cleared.

Here’s the part that surprises most people: the second late payment penalty remains as an estimate until the original debt is cleared. HMRC doesn’t officially realise (or confirm) the final amount until the overdue balance is fully settled. For business owners who have worked hard to pay off a debt, receiving a confirmed penalty at the point of clearance can feel like a punishment for doing the right thing.

What This Means If You're on a Payment Plan

If you’re already managing an overdue VAT liability through a Time to Pay arrangement with HMRC, there’s an important detail worth understanding.

Second late payment penalties cannot be added to a payment plan. They sit outside the arrangement entirely. And because HMRC is not currently allowing new debt to be added onto existing debt within a plan, these penalties can appear to materialise out of nowhere…particularly if you have several different overdue periods being cleared at different points.

As each overdue period within your plan is completed, the second late payment penalty for that period is confirmed and presented separately. If you’re not expecting this, it can feel sudden and disorienting, even when you’ve been doing everything right.

The practical advice here is straightforward: keep your payment plan up to date, stay on top of any current VAT liabilities so they don’t fall into overdue status, and pay any penalties as they are confirmed. This matters because penalties also accrue interest, so leaving them unpaid adds to your overall cost.

Why This Can Trigger a Wider HMRC Investigation

It’s worth being aware that if penalties and interest grow large enough (particularly outside of a payment plan) this can trigger a broader HMRC compliance review. It can also put any existing payment plan at risk of being cancelled.

This is one of the reasons staying on top of penalties promptly is so important. It’s not just about the cost of the penalties themselves, it’s about protecting the broader arrangement you have in place.

Four Things Worth Doing If You Have an Overdue VAT Liability

Act quickly as the 15-day window matters:

If you know a VAT payment is going to be late, paying within 15 days avoids the penalty charge entirely. Even if you can’t pay in full, getting in touch with HMRC promptly demonstrates good faith and opens the door to a payment arrangement before penalties escalate.

Understand what you owe in full:

Make sure you have a clear picture of not just the original VAT liability but any interest and penalties that have accrued. It’s easy to focus on the headline figure and overlook the additional charges building alongside it.

Keep any payment plan current:

If you’re on a Time to Pay arrangement, staying up to date with every payment is critical. Falling behind on the plan itself can trigger cancellation, and with it, the full outstanding balance becomes due immediately.

Pay penalties as they are confirmed:

When second late payment penalties are realised, pay them promptly. They accrue interest in the same way as the original liability, and leaving them unresolved adds to the overall cost and increases the risk of triggering a compliance review.

Frequently Asked Questions

Don’t wait and hope it resolves itself. If you can pay within 15 days of the due date, do so immediately as that window removes the penalty charge entirely. If you can’t pay in full, contact HMRC as soon as possible to discuss your options. Acting quickly almost always leads to a better outcome than waiting.

Your HMRC online account should reflect your current liability, but it doesn’t always show the full picture, particularly around second late payment penalties which remain as estimates until the debt is cleared. Your accountant can help you build a complete picture of what you owe and what may still be confirmed once payments are made.

In some circumstances, yes. HMRC does have a process for appealing penalties where there is a reasonable excuse for example, a serious illness or an event genuinely outside your control. General cash flow difficulties are unlikely to be accepted as a reasonable excuse, but it’s always worth discussing your specific situation with your accountant before assuming there’s no room for movement.

The most effective approach is treating VAT as ring-fenced from the moment it’s collected, setting it aside rather than using it as working capital. Building your VAT due date into your cash flow planning well in advance, and flagging any potential shortfall to your accountant early, means you’re never caught off guard.

Final Thoughts

The VAT penalty system is more layered than most business owners realise and the costs can escalate quickly, particularly once a liability moves past the 30-day mark.

The good news is that for businesses who act promptly, communicate openly with HMRC and stay on top of their payment obligations, the system is manageable. The key is understanding how it works before you find yourself in it…not after.

If you’re currently managing an overdue VAT liability, have concerns about penalties that have accrued, or simply want to make sure your VAT position is well managed going forward, we’re always happy to talk it through. We’re not just here at year-end or when something goes wrong but through every decision, challenge and milestone along the way.

Simply get in touch to chat with a member of our team today!